Executive Summary (BLUF): In the current Q2 2026 credit environment, the choice between Senior Secured Bonds and Revolving Credit Facilities (RCFs) is no longer a matter of interest rate arbitrage, but a survival strategy against “Capital Immobilization.” For Dry Bulk operators in the USA, UAE, and UK, shifting toward long-tenor bond structures is the only viable hedge against the sudden “Loan Recalls” currently being triggered by commercial banks under Basel IV RWA (Risk-Weighted Asset) constraints.

1. The Economic Impact: Protecting Balance Sheet Liquidity from “Regulator Erosion”

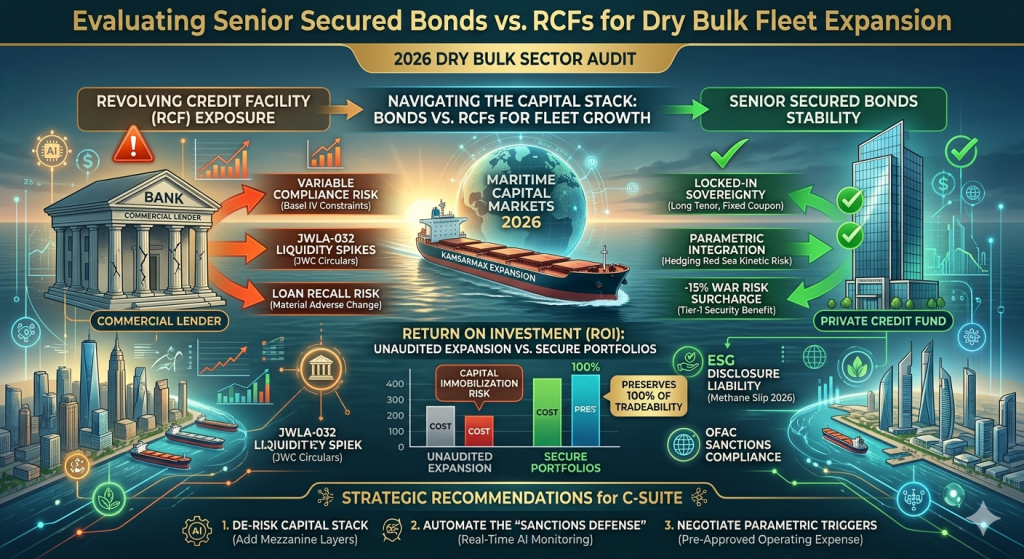

For institutional investors, the Dry Bulk sector in 2026 presents a paradox: high demand for “Green” mineral transport coupled with unprecedented Asset Seizure & Hull War Risk. Choosing a traditional RCF (Revolving Credit Facility) today introduces a “Variable Compliance Risk.” Because RCFs are typically held by commercial banks, a single unfavorable Joint War Committee (JWC) Circular, such as the recent JWLA-032, can lead to a lender freezing your facility to lower their own risk exposure.

The Bond Advantage in a Kinetic Market

By contrast, Senior Secured Debt in the form of high-yield maritime bonds provides “Locked-In Sovereignty.” While the coupon may be higher than a floating-rate RCF, bonds insulate the shipowner from the “Covenant Contagion” seen in 2026. If your fleet is forced to navigate the Red Sea, an RCF lender might demand an immediate injection of equity to cover the spike in Parametric Insurance Premiums. A bond structure, however, allows the operator to maintain liquidity during high-volatility events, preserving the IRR of the expansion project.

2. The Compliance/Legal Framework: The “Triple Threat” of 2026

Expanding a Dry Bulk fleet in 2026 requires navigating three distinct legal minefields that directly impact debt serviceability:

- The Methane Slip & EU ETS Nexus: 2026 marks the first full year where methane slip—not just —is factored into EU ETS costs. For dual-fuel Dry Bulk vessels, this ESG Disclosure Liability is now a senior-ranking debt. Failure to account for this in your cash-flow modeling can lead to a technical default on your senior debt.

- JWLA-032 and Geographic Exclusion: The Joint War Committee (JWC) Circulars have expanded the “Listed Areas” to include new corridors in the Indian Ocean. RCF lenders are increasingly using these circulars to trigger “Material Adverse Change” (MAC) clauses, effectively seizing control of vessel routing.

- OFAC Sanctions Compliance in the “Middle Corridor”: With the rise of the shadow fleet, Dry Bulk operators transiting UAE hubs must maintain forensic OFAC Sanctions Compliance trails. Bonds often have more predictable compliance reporting cycles compared to the intrusive, weekly “Know Your Cargo” audits now required by RCF providers.

3. Strategic Recommendations: 3 Actionable Steps for the CEO

I. De-risk the Capital Stack with Mezzanine Layers

Do not fund a 2026 expansion solely through senior bank debt. Utilize a hybrid approach: Layer Senior Secured Debt (Bonds) with a 15% Mezzanine Financing slice. This “buffer capital” allows you to absorb sudden spikes in Hull War Risk premiums without breaching your primary debt covenants.

II. Automate the “Sanctions Defense”

Integrate AI-driven navigation and monitoring systems to mitigate Arbitration & Litigation Costs. In the Red Sea, where “Kinetic Liability” is high, having an immutable digital log of your vessel’s proximity to sanctioned entities is the only way to satisfy the “Due Diligence” requirements of Tier-1 bondholders.

III. Negotiate Parametric Triggers into Debt Covenants

Move away from “Indemnity-based” insurance as your only hedge. Work with your Lead Underwriter to include Parametric Insurance Premiums as a pre-approved operating expense in your bond prospectus. This ensures that if a JWC-listed event occurs, the immediate cash payout maintains your debt service coverage ratio (DSCR).

Frequently Asked Questions (FAQ)

1. Why are Senior Secured Bonds preferred over RCFs for UAE-based expansion?

UAE-based founders often face “Secondary Sanctions” scrutiny from Western commercial banks. Senior Secured Bonds, often placed with private credit funds or institutional investors in the UK and USA, provide a more stable, long-term commitment that isn’t subject to the reactionary “de-risking” whims of a commercial bank’s compliance desk.

2. How does the JWLA-032 circular impact my “Cost of Debt”?

JWLA-032 expanded the high-risk zones. For RCF holders, this often triggers an automatic hike in the margin (spread) above LIBOR/SOFR to compensate the bank for increased risk. For bondholders, the interest rate is fixed, meaning your only variable cost is the Hull War Risk premium, not the underlying cost of the capital itself.

3. What is the “Methane Slip” trap in 2026 fleet expansion?

Many Dry Bulk owners expanded into LNG-ready ships. However, the 2026 EU ETS phase-in for methane slip means these “cleaner” ships are facing unexpected carbon taxes. If your RCF covenants didn’t account for this ESG Disclosure Liability, you may find your “Free Cash Flow” insufficient to meet monthly RCF repayments.

4. Is AI-driven navigation a liability or an asset for debt securing?

In 2026, it is both. While it reduces the risk of human error in the Red Sea, it introduces new Arbitration & Litigation Costs if the AI deviates from a chartered route. Tier-1 bondholders now require a “Human-in-the-Loop” certification to ensure the insurance remains valid during AI-assisted transits.

5. Can Mezzanine Financing help avoid Asset Seizure?

Yes. In a distressed scenario where a senior lender (RCF) threatens to seize a vessel due to a covenant breach, Mezzanine Financing providers often have “Cure Rights.” They can step in, pay the arrears, and prevent a fire-sale or Asset Seizure, protecting the equity holder’s remaining value.

Expert Advisory for 2026 Maritime Capital Markets

Navigating the transition from bank-led RCFs to Senior Secured Debt & Mezzanine Financing requires a granular understanding of Joint War Committee (JWC) Circulars and OFAC Sanctions Compliance. Investors must engage with Professional Advisory Services to quantify their ESG Disclosure Liability and secure Specialized Insurance Cover that includes Parametric Insurance Premiums. Without a forensic approach to Hull War Risk and Arbitration & Litigation Costs, your fleet expansion remains vulnerable to the systemic liquidity shifts of 2026.

Recent Comments