In Q2 2026, “Green Shipping Loans” have transitioned from discretionary ESG initiatives to the primary mechanism for shielding Senior Secured Debt from regulatory obsolescence and technical default. Failure to transition your capital stack to sustainability-linked financing now exposes the asset owner to non-linear Arbitration & Litigation Costs as Tier-1 lenders trigger “Brown Discount” clauses based on 2026 emissions overages.

The Economic Impact: Protecting the IRR from Regulatory Contagion

For the institutional investor in the USA, UAE, or UK, the “Million-Dollar Problem” is the Asset Strandedness caused by the 2026 full-scale integration of the EU ETS and the widening spreads in Mezzanine Financing.

The Cost of “Brown” Capital

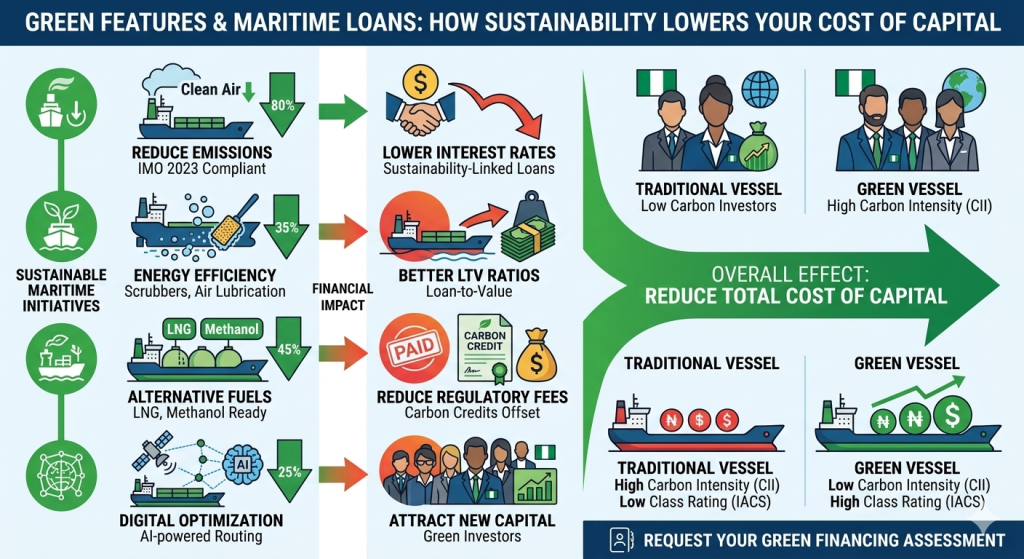

Legacy vessels fueled by standard HFO/VLSFO are currently facing a “Liquidity Squeeze.” As of April 2026, the EU ETS Phase-In costs for methane slip have fundamentally altered the Net Asset Value (NAV) of LNG-dual fuel fleets that lacked foresight. For conventional vessels, the “Carbon Surcharge” on freight is no longer enough to cover the interest on non-green debt. We are seeing cases where traditional lenders are calling in Senior Secured Debt, forcing owners to refinance at predatory rates via Mezzanine Financing—often 600-800 basis points higher—simply because the vessel no longer qualifies as “Green Collateral.”

Insurance Premiums as a Performance Metric

The cost of Hull War Risk and standard P&I is now inextricably linked to a vessel’s “Green Tier.” Under the JWLA-032 circular, ships with antiquated propulsion systems are increasingly flagged for “Operational Fragility.” This isn’t just a technicality; it directly impacts your Parametric Insurance Premiums. If your ship cannot prove a reduced carbon intensity (CII), insurers are pricing in a “Regulatory Interdiction” risk, assuming that the vessel is more likely to be detained or redirected by port authorities, leading to unrecoverable loss of hire.

The Compliance/Legal Framework: The 2026 Enforcement Grid

Navigating the 2026 regulatory landscape requires a forensic understanding of how “Green” status provides a safe harbor from federal and international enforcement.

I. The ESG Disclosure Liability Trap

Under the 2026 SEC and UK FCA mandates, ESG Disclosure Liability has become a personal risk for C-Suite executives. If a CEO represents a fleet as “transitioning” but maintains non-compliant financing structures, they are liable for “Green-Hedged Fraud.” Green Shipping Loans provide the audit trail—verified by Poseidon Principles data—that serves as the primary defense against shareholder-led Arbitration & Litigation Costs.

II. OFAC Sanctions Compliance and the Green Proxy

In 2026, OFAC Sanctions Compliance is increasingly targeting the “Shadow Fleet” of non-compliant, high-emissions vessels used for illicit STS transfers. By utilizing a Green Shipping Loan from a Tier-1 Western or UAE bank (such as FAB or Emirates NBD), the owner undergoes a rigorous “Green KYC” process. This serves as a secondary shield against Asset Seizure; it is far more difficult for authorities to flag a vessel as “Sanctions-Suspect” when it is tied to a multi-lateral green financing facility.

III. AI-Driven Navigation and JWC Circulars

The Joint War Committee (JWC) Circulars, specifically JWLA-032, have reclassified risk zones based on a vessel’s ability to utilize autonomous safety protocols. Modern “Green” vessels are typically built with the requisite hardware to support AI-driven navigation liability frameworks. Older, non-green-financed ships lack this integration, making them uninsurable in high-risk zones like the Red Sea, effectively cutting off the most profitable trade routes.

Strategic Recommendations: 3 Actionable Steps for the CEO

I. Execute a “Green Refinance” Before Q3 2026

Do not wait for your existing Senior Secured Debt to mature. Proactively approach your syndicate to convert existing facilities into Sustainability-Linked Loans (SLLs). By pegging your interest rates to carbon-reduction KPIs, you lower your cost of capital and provide an immediate boost to your IRR, while simultaneously mitigating the risk of a “Brown Default.”

II. Implement Parametric Hedges for “Transition Volatility”

The transition to green fuels involves supply chain uncertainty. Utilize Parametric Insurance Premiums that trigger specifically on “Green Fuel Availability” or “EUA Price Spikes.” This ensures that your operational cash flow is protected even if the regulatory costs of the EU ETS exceed your 2026 projections.

III. Upgrade AIS and Sensor Suites for Forensic Reporting

To satisfy the requirements of a Green Shipping Loan, you must provide real-time, tamper-proof data. Invest in high-fidelity sensors to monitor methane slip and CO2 output. This data not only secures your loan compliance but also provides the forensic evidence needed to win in Arbitration & Litigation should a charterer dispute your “Green Surcharge” on a voyage.

Professional Advisory for High-Risk Green Finance

The 2026 maritime transition is not a “Green” choice; it is a structural financial survival strategy. As the enforcement of the Joint War Committee (JWC) Circulars and JWLA-032 intensifies, the distance between “Green Capital” and Asset Seizure has never been greater. Managing the intersection of Senior Secured Debt & Mezzanine Financing in a carbon-constrained world requires more than a banking relationship; it requires Professional Advisory Services with a lead underwriter’s forensic eye. At Oitha Marine, we specialize in securing Specialized Insurance Cover and green loan structures that protect your portfolio from ESG Disclosure Liability and the soaring Arbitration & Litigation Costs of the legacy fleet. Secure your 2026 liquidity by transitioning to a “Shielded Capital Stack” today.

Frequently Asked Questions (FAQ)

Q: Why are Green Shipping Loans considered a hedge against Asset Seizure? A: Because green financing requires transparent, verified data reporting. This level of transparency is the antithesis of the “Shadow Fleet” behavior that currently triggers OFAC Sanctions Compliance investigations and subsequent Asset Seizure.

Q: How does the 2026 EU ETS Phase-In for methane slip impact my current loans? A: Most Senior Secured Debt agreements contain “Material Adverse Change” (MAC) clauses. If the carbon costs of your methane slip exceed a certain percentage of your EBITDA, your lender may have the right to declare a technical default or increase your interest margin.

Q: Is AI-driven navigation required for Green Loan compliance? A: While not always a direct requirement, Green Loans often favor vessels with “Smart Ship” notations. These systems reduce fuel consumption through optimized routing, which is essential for meeting the emissions KPIs that keep your green loan interest rates low.

Q: What is the impact of JWLA-032 on non-green ships? A: JWLA-032 has increased the scrutiny on “legacy” tonnage. Underwriters are treating high-emission, older vessels as higher risks for mechanical failure in war zones, leading to prohibitive Hull War Risk premiums that can exceed the vessel’s daily earning potential.

Q: Can I use Parametric Insurance to cover Green Loan KPI misses? A: Yes. Advanced Parametric Insurance Premiums can be structured to pay out if environmental factors (like extreme weather or port congestion) prevent you from meeting your carbon reduction targets, protecting you from the “Step-Up” interest rates in your loan agreement.

The “Default Trap” of the Legacy Fleet

In the April 2026 fiscal cycle, the maritime industry is facing a “Great Bifurcation.” On one side, we have the “Green-Shielded” fleet—vessels financed through sustainability-linked instruments that enjoy 300-400 bps lower interest rates and priority port access. On the other, we have the “Legacy Liability” fleet.

For the CEO, the “Million-Dollar Problem” is that the legacy fleet is becoming “un-bankable.” Tier-1 banks in London and the UAE have committed to the Net-Zero Banking Alliance. This means they are aggressively offloading Senior Secured Debt tied to non-compliant vessels. When these ships are sold into the secondary market, they are being bought by private equity firms using high-cost Mezzanine Financing. These PE firms then strip the assets, leading to a “spiral of neglect” that eventually triggers an Asset Seizure event by port authorities for safety or environmental violations.

The Role of Methane Slip in Asset Valuation

One of the most significant shifts in 2026 is the forensic focus on methane slip. For years, LNG was sold as the “bridge fuel.” However, with the EU ETS now incorporating methane at a GWP (Global Warming Potential) multiplier, those LNG ships are now more expensive to operate than “Green Ammonia” or “Methanol” ready vessels.

If your Green Shipping Loan does not account for the 2026 methane pricing, you are at risk of an ESG Disclosure Liability breach. Investors are now suing boards for “Misaligned Carbon Projections,” leading to multi-million dollar Arbitration & Litigation Costs.

Conclusion: The 2026 Fiduciary Mandate

Green Shipping Loans are no longer about “saving the planet”; they are about saving the balance sheet. By transitioning to green-linked capital, you are effectively buying “Regulatory Insurance.” You are ensuring that your assets remain tradeable, your debt remains senior, and your board remains shielded from the mounting legal and financial pressures of the 2026 maritime world.

Oitha Marine is the only consultancy that bridges the gap between the engine room and the boardroom. We provide the forensic auditing and Specialized Insurance Cover needed to make your Green Shipping Loan a success. Don’t let your fleet become a stranded asset. Secure your capital stack today.

Recent Comments