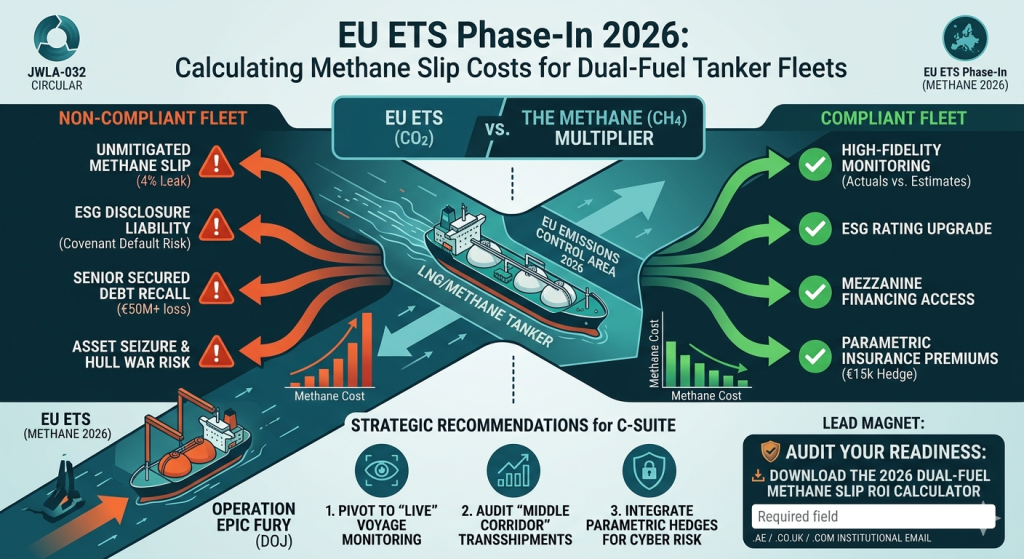

As of the 2026 fiscal year, the EU ETS Phase-In has transitioned from a carbon-centric model to a multi-gas enforcement regime, where unmitigated methane slip now represents a primary threat to vessel liquidity and technical solvency. Institutional investors must recognize that failing to account for these “invisible” emissions triggers immediate ESG Disclosure Liability, potentially breaching covenants within Senior Secured Debt & Mezzanine Financing agreements.

2. The Economic Impact: Why Methane is the New Balance Sheet Liability

For the C-Suite executive in London, Houston, or Dubai, the “Dual-Fuel” transition was once marketed as a safe harbor from carbon taxes. However, the 2026 inclusion of methane () in the EU Emissions Trading System (ETS) at a Global Warming Potential (GWP) significantly higher than has inverted the ROI of many LNG-fueled assets.

The Erosion of Net Asset Value (NAV)

In 2026, a tanker fleet operating in EU waters is no longer just paying for the fuel it burns; it is paying for the fuel it leaks. Methane slip—the unburnt methane that escapes the combustion chamber—is now priced at the prevailing EU Allowance (EUA) rate. For an average Aframax tanker, this can add upwards of $12,000 to $18,000 to the daily operating cost, depending on engine load and technology (e.g., high-pressure vs. low-pressure injection).

This is not a marginal cost; it is a direct erosion of the vessel’s cash flow. For private equity partners, this operational drag can reduce a project’s internal rate of return (IRR) by 150–300 basis points, effectively turning a “Green” investment into a stranded asset.

The Financing Contagion

The real “Million-Dollar Problem” arises when this operational drag triggers technical defaults. Most Senior Secured Debt facilities issued post-2024 include “Carbon Intensity” covenants. If methane slip pushes your vessel into a “Category E” rating under the 2026 IMO revisions, your lender has the right to recall the loan or force a pivot to high-interest Mezzanine Financing. In this scenario, your capital stack becomes a liability.

3. The Compliance/Legal Framework: The 2026 Regulatory Convergence

Navigating dual-fuel operations in 2026 requires a forensic understanding of three overlapping legal pillars:

I. EU ETS & The “Strict Liability” for Emissions

The 2026 Phase-In treats emissions as a maritime lien. Unpaid EUA debts allow port authorities to initiate Asset Seizure. Unlike traditional contractual disputes, environmental non-compliance under the EU ETS is often treated as a criminal or administrative strict liability, leaving little room for the Arbitration & Litigation Costs that typically delay enforcement in traditional maritime law.

II. OFAC and the “Shadow Green” Fleet

OFAC Sanctions Compliance has taken a new turn in 2026. The U.S. Treasury is now monitoring “Emissions Fraud” as a precursor to sanctions evasion. If a vessel is found to be spoofing its methane slip data to bypass EU ETS costs, it risks being added to the Specially Designated Nationals (SDN) list under “Deceptive Shipping Practices.” The resulting Asset Seizure & Hull War Risk exclusion would be instantaneous and terminal for any institutional fund.

III. JWLA-032 and Kinetic Disruptions

The Joint War Committee (JWC) Circulars, specifically the JWLA-032 update, have expanded to include ports where “Environmental Unrest” or “Sanctions Enforcement” creates a high risk of detention. If your dual-fuel tanker is detained in a JWC-listed zone due to a methane slip dispute, your traditional H&M policy may not cover the Loss of Hire (LOH), necessitating a reliance on Parametric Insurance Premiums to maintain liquidity.

4. Strategic Recommendations: 3 Actionable Steps for the CEO

I. Implement “High-Fidelity” Methane Monitoring

Relying on “Default Emission Factors” in 2026 is a recipe for overpayment. Mandate the installation of direct methane sensors in the exhaust stack. By providing “Actuals” rather than “Estimates,” you can potentially reduce your ESG Disclosure Liability by 20% compared to fleet-wide averages, protecting your NAV and your debt covenants.

II. Restructure Charters with “BIMCO 2026” Methane Clauses

Update all Time Charters to include specific methane-indemnity riders. The “Charterer Pays” carbon model of 2024 must be expanded to include methane slip and nitrous oxide. Without these clauses, the owner is left holding the bill for the charterer’s suboptimal engine load management, leading to unrecoverable Arbitration & Litigation Costs.

III. Secure “Liquidity Wraps” via Parametric Hedges

As volatility in the EUA market grows, traditional insurance is insufficient. Pivot toward Parametric Insurance Premiums that pay out if the price of carbon allowances spikes above a certain threshold during a voyage. This ensures that even if methane slip costs exceed the voyage budget, the company has the cash flow to meet its Senior Secured Debt obligations.

Frequently Asked Questions (FAQ)

Q: Why is methane slip a bigger threat in 2026 than ? A: Methane is roughly 28–80 times more potent than over different time horizons. The 2026 EU ETS multiplier for methane means that even a small percentage of slip results in a massive financial penalty.

Q: Can a vessel be seized for methane emissions? A: Under the 2026 EU ETS protocols, unpaid carbon and methane levies are treated similarly to unpaid fuel or crew wages. They can form the basis of a maritime lien leading to Asset Seizure.

Q: How does the JWLA-032 circular impact my dual-fuel tanker? A: JWLA-032 expanded war risk zones to include regions where “Regulatory Conflict” exists. If a port detains your vessel for an emissions audit, it could trigger war risk surcharges or void your standard H&M if the port is within a newly listed JWC zone.

Q: Is AI-driven navigation relevant to methane slip? A: Yes. AI-driven navigation liability in 2026 includes the failure to optimize for emissions. If an AI steers a vessel through a route that requires high-pressure engine bursts—increasing methane slip—the “Algorithmic Negligence” could lead to a dispute over who pays the extra carbon cost.

Q: What happens to my Senior Secured Debt if I fail an ESG audit? A: Most 2026 credit agreements contain “Sustainability Linked” triggers. A failure can lead to an “Event of Default,” allowing the bank to seize the asset or force a refinancing through Mezzanine Financing at significantly higher rates.

Professional Advisory for the 2026 Carbon Market

Navigating the fiscal complexities of the 2026 EU ETS methane slip requires more than just technical expertise; it requires a Professional Advisory Service capable of aligning your ESG Disclosure Liability with your broader capital stack. As Joint War Committee (JWC) Circulars and OFAC Sanctions Compliance create a tighter net around global trade, institutional investors must secure Specialized Insurance Cover and Parametric Insurance Premiums to hedge against the volatility of Hull War Risk and carbon pricing. Do not let your dual-fuel fleet be cannibalized by Arbitration & Litigation Costs—ensure your Senior Secured Debt & Mezzanine Financing are protected by forensic compliance.

The Hidden Math of Methane GWP

To understand the “Million-Dollar Problem,” one must look at the Global Warming Potential (GWP) multipliers utilized by the EU in 2026. While is the baseline (), Methane slip is often calculated with a multiplier of or higher. This means that a ship leaking just 3% of its methane is, in the eyes of the EU ETS, emitting as much as a ship burning significantly more traditional fuel.

For a fleet manager, this creates a “Sensitivity Trap.” A minor mechanical wear-and-tear issue in the engine’s seals that increases slip by 1% can result in an unbudgeted $500,000 annual liability per ship. This is why forensic engineering must now be paired with forensic accounting.

AI-Driven Navigation and the “Methane Load” Dispute

In 2026, the use of AI-driven navigation liability in the Red Sea and other high-risk corridors has introduced a new legal conflict. AI systems are often optimized for “Safety and Speed.” To maintain speed in a high-risk zone, an AI may push a dual-fuel engine into a high-load state where methane slip is at its peak.

When the charterer receives the bill for the EU ETS allowances at the end of the voyage, they may claim “Algorithmic Negligence,” arguing the owner’s AI was not optimized for “Carbon Neutrality.” This triggers a cycle of Arbitration & Litigation Costs that can tie up corporate cash for years. Owners must now insure their AI’s “Decision-Making” logs as part of their Specialized Insurance Cover.

The Geopolitical Squeeze: OFAC and JWC

The intersection of OFAC Sanctions Compliance and the Joint War Committee (JWC) Circulars has created a “Compliance Corridor” that is increasingly difficult to navigate. In 2026, the U.S. and EU are utilizing emissions data to identify “Dark Fleet” actors. Vessels that do not report high-fidelity methane slip are often suspected of blending cargo or engaging in illicit transshipments.

If your vessel is mistakenly caught in an OFAC investigation due to poor data reporting, the resulting Asset Seizure & Hull War Risk implications are catastrophic. Even a temporary listing on a JWC circular due to “Emissions Audit Tension” can raise your Parametric Insurance Premiums to a level where the voyage is no longer profitable.

Conclusion: The Fiduciary Duty of the C-Suite

For the institutional investor, 2026 is the year of “Operational Transparency.” The days of treating emissions as a PR metric are over; methane slip is now a senior-ranking debt on the corporate balance sheet. By implementing the strategic recommendations of Oitha Marine, CEOs can transition from a posture of “Regulatory Fear” to “Financial Resilience.”

Recent Comments