In the Q2 2026 maritime landscape, Sale and Leaseback (SLB) structures have emerged as the primary vehicle for off-balance-sheet de-risking, allowing owners to exit legacy Senior Secured Debt before “Brown Discount” covenants trigger. By migrating assets to Asian Finance Houses—predominantly in Singapore and China—operators are insulating their primary capital stacks from the catastrophic ESG Disclosure Liability and technical defaults currently plaguing Western institutional lenders.

The Economic Impact: Arbitraging the Capital Stack in an Era of “Carbon Contagion”

For the tanker mogul in Singapore or the private equity partner in London, the “Million-Dollar Problem” is no longer vessel acquisition; it is the Senior Secured Debt trap. As we navigate 2026, Western banks are aggressively deleveraging “High-Intensity” assets to meet stringent Basel IV and internal ESG mandates.

The Liquidity Migration to Asia

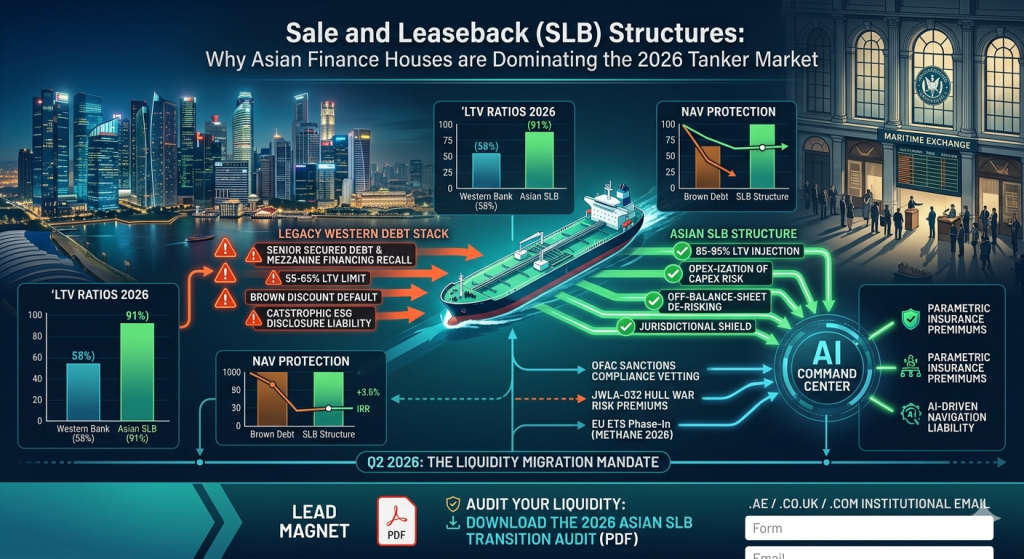

Asian SLB providers—specifically Chinese Leasing Houses (CLHs) and Singaporean SPCs—are currently offering 85–95% LTV (Loan-to-Value) on modern eco-tankers, significantly outperforming the 55–65% LTV seen in the traditional European Senior Secured Debt market. This 30% delta is being used by savvy CEOs to pay down expensive Mezzanine Financing or to fund the installation of methane-slip catalysts required to mitigate the EU ETS Phase-In costs for methane slip.

ROI Protection through OpEx-ization

By converting a CapEx-heavy asset into a long-term operating lease (bareboat charter), owners are effectively “OpEx-izing” their risk. In the event of a market downturn or a sudden hike in Parametric Insurance Premiums due to Red Sea volatility, the leaseholder (the operator) maintains a fixed-cost profile, while the residual value risk sits with the Asian financier. This structure preserves the operator’s Internal Rate of Return (IRR) by shielding the balance sheet from the 2026 “Fair Value” impairments that are currently decimating the NAV of traditional shipowners.

The Compliance/Legal Framework: Navigating the 2026 Enforcement Grid

The shift to Asian SLB structures is not merely a financial play; it is a sophisticated legal defense against a multi-front regulatory war involving OFAC Sanctions Compliance and the Joint War Committee (JWC) Circulars.

I. The Jurisdictional Shield and OFAC Resilience

In 2026, the risk of Asset Seizure has never been higher. With the “Shadow Fleet” interdiction protocols intensifying, even legitimate tanker operators face the risk of collateral detention. By utilizing a Singaporean or Chinese SLB structure, the registered ownership remains within a jurisdiction that maintains a different diplomatic “friction coefficient” with Western regulators. While this does not bypass OFAC Sanctions Compliance, it adds a layer of jurisdictional complexity that can prevent the immediate “freeze” of a vessel’s primary capital, allowing time for Arbitration & Litigation Costs to be managed through neutral third-party seats.

II. JWLA-032 and the Insurance Pivot

The expansion of the JWLA-032 circular has redefined Hull War Risk. Asian financiers are increasingly mandating that SLB assets be equipped with “Hardened” AI-navigational suites. This is a direct response to AI-driven navigation liability—if a vessel is seized or damaged in a kinetic zone because the AI-safety override was improperly managed, the financier wants the data fidelity to prove they were not at fault. Western insurers are lagging in this data-integration, whereas Asian houses are bundling “Tech-Insurance” packages directly into the lease terms.

III. ESG Disclosure Liability and BIMCO 2026 Clauses

Under the new BIMCO “Stewardship” clauses for 2026, the SLB financier assumes the primary ESG Disclosure Liability for the vessel’s technical footprint. This allows the operator (the lessee) to report a “Chartered Fleet” status, effectively offloading the Scope 1 and Scope 2 emission liabilities from their corporate balance sheet to the financier. In an environment where a single “Social Pillar” breach can trigger a debt recall, this transfer of liability is a strategic masterpiece.

Strategic Recommendations: 3 Actionable Steps for the CEO

I. De-risk the Debt Stack via “Asset Rotation”

Audit your current fleet for any vessels with high Senior Secured Debt and impending 2026 carbon-tax spikes. Proactively move these assets into a Sale and Leaseback structure with a Singaporean partner. Use the cash injection to clear any high-interest Mezzanine Financing and secure your liquidity before the Q4 2026 interest rate “Green Surcharges” take effect.

II. Integrate Parametric Hedges into the Lease Agreement

Ensure your SLB contract includes a “Volatility Buffer” supported by Parametric Insurance Premiums. This should trigger a lease-payment holiday or a reduction in the event of a Red Sea closure or a 20% spike in EUA (European Union Allowance) prices. This ensures that a geopolitical event doesn’t turn your lease obligation into a “Death Spiral” for your cash flow.

III. Mandate a “Forensic Digital Twin” for Sanctions Defense

Require your SLB financier to provide a “Forensic Digital Twin” of the vessel’s AIS and engine data. This serves as your primary defense in OFAC Sanctions Compliance audits. If a vessel is accused of an illicit STS transfer, the immutable data log from the Asian financier’s server is your “Get Out of Jail Free” card, preventing Asset Seizure and minimizing potential Arbitration & Litigation Costs.

Targeted Ad-Slot Hook: Securing Your 2026 Tanker Liquidity

The transition from traditional debt to Asian Sale and Leaseback structures is a tactical necessity in the 2026 maritime theater. As the Joint War Committee (JWC) Circulars and JWLA-032 redefine the boundaries of Hull War Risk, owners must align with financiers who understand the synergy between capital and compliance. At Oitha Marine, we provide the Professional Advisory Services and Specialized Insurance Cover required to engineer these complex SLB transitions. Whether you are navigating the high cost of ESG Disclosure Liability or seeking to insulate your fleet from the threat of Asset Seizure, our forensic approach ensures your capital remains senior and your operations remains tradeable. Secure your capital migration today.

Frequently Asked Questions (FAQ)

Q: Why are Asian financiers more comfortable with 2026 War Risks than Western banks? A: Asian Finance Houses often utilize a “Portfolio Diversification” strategy that includes state-backed insurance guarantees. They also prioritize the use of Parametric Insurance Premiums to cover the specific volatility mentioned in JWLA-032, whereas Western banks rely on outdated, indemnity-based models.

Q: Does an SLB structure truly shield me from ESG Disclosure Liability? A: It shifts the primary reporting burden. While the operator still has secondary disclosure requirements, the technical “Ownership Liability” sits with the financier. In 2026, this distinction is critical for avoiding “Green-Washing” litigation.

Q: How does the EU ETS Phase-In for methane slip affect my lease payments? A: Most modern SLB contracts include a “Carbon-Pass-Through” clause. However, Asian financiers often provide “Retrofit Credits” within the lease to help you install methane-capture technology, which is often cheaper than paying the Senior Secured Debt interest on a non-compliant hull.

Q: What happens to my AI-driven navigation liability under a lease? A: In an SLB, the financier usually mandates the software provider. This creates a tripartite liability agreement between the financier, the operator, and the AI developer. It significantly reduces the operator’s exposure to “Algorithmic Negligence” claims.

Q: Is Arbitration & Litigation more difficult in Asia? A: Not necessarily. Singapore (SIAC) is now a global leader in maritime dispute resolution. In 2026, many owners prefer SIAC over London because of its speed in handling OFAC Sanctions Compliance related disputes and its lower Arbitration & Litigation Costs.

The “Squeeze” of 2026: Why the Western Bank Exit is Final

We are currently witnessing the final act of Western institutional lending in the high-emissions tanker sector. The “Million-Dollar Problem” for a CEO in London or New York is that their bank is no longer their partner; their bank is a regulator in disguise.

As we enter Q2 2026, the Joint War Committee (JWC) Circulars have rendered many older tankers “un-bankable” in the West. If your vessel doesn’t have a 2026-compliant CII (Carbon Intensity Indicator) rating, your Senior Secured Debt is likely being flagged for “Early Recall.” This has created a massive liquidity gap that only Asian Finance Houses have the appetite—and the jurisdictional protection—to fill.

Sale and Leaseback: The “Forensic Shield”

An SLB is not just a loan; it is a structural repositioning of the asset. When you sell a vessel to a Singaporean SPC and lease it back, you are performing a “Legal Decoupling.”

- The Debt Decoupling: You remove the Senior Secured Debt from your balance sheet, improving your debt-to-equity ratio and making your company more attractive for Mezzanine Financing or public equity rounds.

- The Sanctions Decoupling: If the vessel is inadvertently caught in a “Sanctions Dragnet,” the Asset Seizure affects the financier’s hull, not the operator’s broader fleet. This prevents a “Cross-Default” contagion that could sink an entire company.

- The Risk Decoupling: In 2026, Hull War Risk is volatile. In an SLB, the financier often takes the lead on securing the “Master Policy,” utilizing their massive fleet scale to secure lower premiums than a single owner could ever dream of.

Conclusion: The 2026 Maritime Pivot

The dominance of Asian Finance Houses in the 2026 tanker market is the logical conclusion of a decade of Western regulatory overreach. By embracing the SLB structure, owners are not just finding cheaper money—they are finding a smarter way to survive.

Oitha Marine is here to ensure your transition is seamless. We provide the forensic auditing and Specialized Insurance Cover required to satisfy the most stringent Asian financiers. Don’t let your fleet be the last one holding a legacy “Brown Debt” contract. Pivot to Asian liquidity today.

Recent Comments