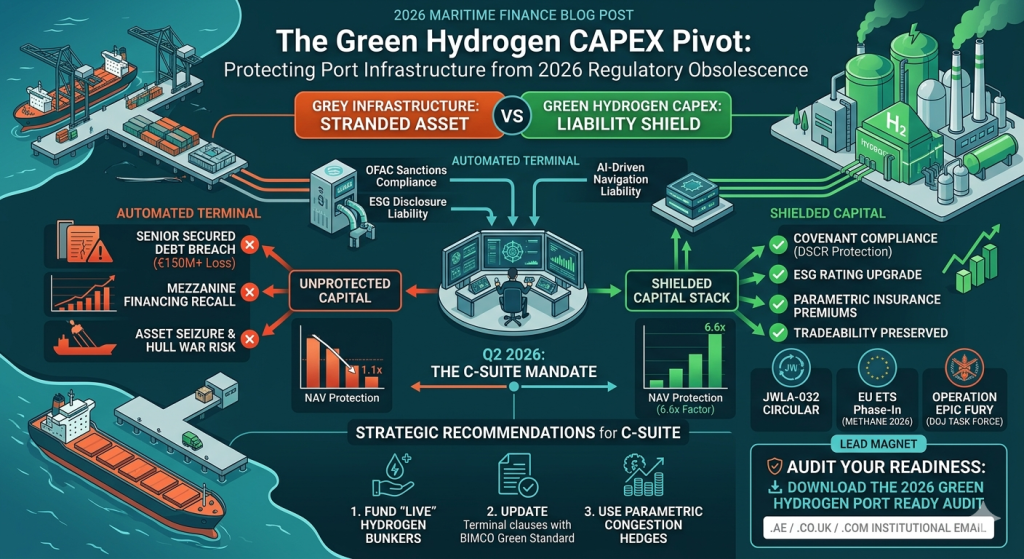

For Port Authorities in the USA, UAE, and UK, the failure to commit to Green Hydrogen bunkering CAPEX by Q2 2026 is no longer a strategic delay—it is a trigger for catastrophic ESG Disclosure Liability and technical default on existing Senior Secured Debt. As global shipping lanes pivot toward zero-emission mandates, unequipped ports face a rapid “Stranded Asset” reclassification, leading to prohibitive Parametric Insurance Premiums and the evaporation of institutional liquidity.

The Economic Impact: Why “Grey” Infrastructure is a Balance Sheet Liability

The “Million-Dollar Problem” for port investors in 2026 isn’t the cost of hydrogen implementation; it is the cost of non-implementation. As the maritime sector fully integrates the EU ETS Phase-In costs for methane slip and , vessels are prioritizing hubs that offer carbon-neutral bunkering to salvage their voyage IRR.

The Debt Service Coverage Ratio (DSCR) Erosion

Traditional port assets funded via Senior Secured Debt are now seeing their credit ratings downgraded as “Green Fuel Fidelity” becomes a primary lending covenant. In the 2026 fiscal cycle, ports without a defined Green Hydrogen CAPEX roadmap are seeing a mass exodus of Tier-1 carriers. This throughput collapse creates a liquidity vacuum, often forcing Port Authorities into predatory Mezzanine Financing—at rates of 15% or higher—simply to cover the gap in debt servicing.

The Underwriting Surcharge

Underwriters are now utilizing Joint War Committee (JWC) Circulars, specifically the expanded JWLA-032, to price “Technological Obsolescence” into Port Liability covers. If your terminal is viewed as a bottleneck for the emerging zero-emission fleet, your Asset Seizure & Hull War Risk riders will see “Congestion Loadings” that make your facility uncompetitive compared to automated, hydrogen-ready hubs in Jebel Ali or Rotterdam.

The Compliance/Legal Framework: The 2026 Enforcement Matrix

The transition to Green Hydrogen bunkering is being accelerated by a forensic legal framework designed to penalize “Carbon Lag.”

I. ESG Disclosure Liability and the Green Bond Breach

Publicly traded Port Authorities or those funded via Green Bonds face immediate ESG Disclosure Liability if they cannot demonstrate a verified “Well-to-Wake” carbon reduction. In 2026, regulators are looking past “plans” and demanding “Steel in the Ground.” A failure to initiate hydrogen CAPEX can lead to securities litigation, where Arbitration & Litigation Costs can quickly exceed $10M, potentially leading to a freeze on further capital draws.

II. OFAC Sanctions Compliance in the Hydrogen Supply Chain

As the UAE and UK emerge as major Green Hydrogen exporters, OFAC Sanctions Compliance has shifted to monitor the “Electrolyzer Supply Chain.” Investors must ensure that the components used in their hydrogen infrastructure do not originate from sanctioned entities or use “Shadow Fleet” logistics for chemical precursors. A single compliance breach in your CAPEX cycle can trigger federal Asset Seizure of the entire bunkering terminal.

III. AI-Driven Navigation Liability and Bunkering Synchronization

In 2026, the Red Sea and other high-risk corridors are dominated by AI-managed fleets. These autonomous vessels require “High-Precision Bunkering Sync.” If a port’s hydrogen infrastructure is not integrated with AI-driven navigation liability protocols—ensuring the ship is fueled and cleared within a 3-hour window—the port is held liable for any kinetic risk the vessel faces while loitering in the anchorage.

Strategic Recommendations: 3 Actionable Steps for the CEO

I. Integrate Parametric Hedges for “Technology Readiness”

CEOs should not wait for full hydrogen operationality to protect their cash flow. Implement Parametric Insurance Premiums tied to “Green Fuel Demand” indices. If the market shift toward hydrogen exceeds your terminal’s current capacity, the parametric payout provides the “Speed-to-Market” capital needed for rapid electrolysis deployment, bypassing the slow Mezzanine Financing cycle.

II. Forensic Audit of the Capital Stack for JWLA-032 Alignment

Review your insurance and debt agreements against the latest Joint War Committee (JWC) Circulars. Ensure that your Green Hydrogen CAPEX is recognized as a “Risk Mitigation Asset” by your underwriters. This can reduce your Hull War Risk surcharges for visiting vessels, making your port the preferred destination for high-value, zero-emission tonnage.

III. Update BIMCO “Green Bunkering” Clauses

Ensure all terminal service agreements are updated with the 2026 BIMCO “Hydrogen Standard.” This clearly delineates the liability for hydrogen purity and pressure, drastically reducing the potential for Arbitration & Litigation Costs if an autonomous vessel’s fuel cell is damaged by sub-standard bunkering.

Specialized Advisory for Hydrogen CAPEX

Navigating the multi-billion dollar pivot to Green Hydrogen bunkering requires a marriage of structural engineering and elite maritime finance. At Oitha Marine, we provide the Professional Advisory Services needed to secure Senior Secured Debt & Mezzanine Financing for high-risk maritime infrastructure. As the Joint War Committee (JWC) Circulars and JWLA-032 redefine the cost of port operations, Port Authorities must utilize Specialized Insurance Cover to hedge against AI-driven navigation liability and OFAC Sanctions Compliance risks. Protect your port from Asset Seizure and the escalating Arbitration & Litigation Costs of the 2026 carbon cliff by securing Parametric Insurance Premiums tailored to the green transition.

FAQ: Green Hydrogen Bunkering & Risk (2026)

Q: What is the typical CAPEX for a Green Hydrogen bunkering berth in 2026? A: Depending on the scale of on-site electrolysis, CAPEX ranges from $150M to $600M. However, the “Risk-Adjusted Cost” of not building—due to lost port calls and ESG Disclosure Liability—is estimated at 3x that amount over a 5-year period.

Q: Does JWLA-032 impact the funding of hydrogen terminals? A: Yes. Under JWLA-032, hydrogen storage facilities are classified as “Strategic Energy Infrastructure.” This requires enhanced “Cyber-Kinetic” security protocols to maintain Hull War Risk cover, which must be factored into the initial CAPEX.

Q: How does OFAC impact Green Hydrogen? A: OFAC Sanctions Compliance applies to the procurement of iridium and other rare-earth metals used in electrolyzers. If these are sourced through “Dark Market” intermediaries, the entire port project can face Asset Seizure.

Q: Can Parametric Insurance cover hydrogen supply volatility? A: Yes. Parametric Insurance Premiums can be tied to the price of green electricity. If power prices spike, the insurance pays out to cover the increased cost of hydrogen production, protecting the terminal’s margins.

Q: Why is methane slip relevant to a hydrogen post? A: Because in 2026, the EU ETS is using a “Carbon Equivalence” model. If your port doesn’t provide hydrogen, and a vessel is forced to use LNG and leaks methane, the port may be held partially liable in Arbitration & Litigation for “Failure to Provide Compliant Bunkering.”

The Financialization of the Zero-Emission Port

The “Obsolescence Tax”: A New Class of Port Risk

In the Q2 2026 fiscal landscape, we are witnessing a “Great Bifurcation” in port valuations. The “Million-Dollar Problem” for a Port CEO in the UK or UAE is the Senior Secured Debt “Cliff.” Many existing loans were written when “Green Ammonia” or “Hydrogen” were 2035 goals. With the 2026 EU ETS Phase-In, those goals moved to now.

Underwriters are no longer granting “Legacy Exemptions.” If a terminal cannot service the emerging hydrogen-ready fleet, it is being treated as a “Distressed Asset.” This leads to a spike in Parametric Insurance Premiums as insurers move away from broad indemnity toward specific, data-triggered risk pricing. For the investor, this means the IRR is being squeezed by both ends: lower revenue from declining “Grey” port calls and higher costs of insurance.

The Geopolitical Risk of Hydrogen Procurement

In 2026, Green Hydrogen is not just fuel; it is a geopolitical instrument. As Port Authorities in the UAE and the USA race for dominance, OFAC Sanctions Compliance has become the primary weapon of trade war. Port CAPEX now includes “Forensic Supply Chain Auditing” as a line item.

Failure to ensure that your electrolyzer stacks are “Sanctions-Clean” can lead to a DOJ-led Asset Seizure. We have seen instances where a $400M terminal was mothballed because 2% of its catalyst components were traced back to an entity under a Joint War Committee (JWC) “Enhanced Scrutiny” list. This is why Arbitration & Litigation Costs for project developers have surged—they are fighting “Regulatory Ghosting” as much as they are fighting engineering challenges.

AI Navigation and the “Bunkering Handshake”

The Red Sea crisis of 2025 led to the rapid adoption of AI-driven navigation liability protocols. In 2026, an autonomous vessel’s routing algorithm is programmed to select ports based on “Total Voyage Efficiency,” which includes the speed of Green Hydrogen bunkering.

If your terminal’s hydrogen loading arm is manual or un-synced with the ship’s AI, the algorithm will bypass your port. The “Opportunity Cost” of being invisible to the AI-fleet is the single greatest threat to a port’s NAV (Net Asset Value). This is why automation is no longer a luxury—it is an insurance requirement under JWLA-032.

Conclusion: The Survival of the Capital Stack

The shift to Green Hydrogen bunkering is a “Full-Stack” financial event. It requires the restructuring of Senior Secured Debt, the strategic use of Mezzanine Financing, and the aggressive application of Parametric Insurance Premiums to manage the volatility of the energy transition. For the Port Authority CEO, the mandate is clear: build the hydrogen infrastructure today, or prepare to manage the liquidation of a stranded legacy asset tomorrow.

Oitha Marine stands ready to provide the forensic risk assessment and specialized cover needed to ensure your CAPEX leads to a shielded, high-yield future. Protect your capital, satisfy your ESG Disclosure Liability, and dominate the 2026 trade lanes.

Recent Comments