The global maritime ecosystem is an intricate network of capital-intensive assets, fluid trade corridors, and continuous operational risks. For vessel charterers, cargo owners, and supply chain directors, executing transit operations across international and coastal waters introduces exposure to unpredictable perils. From severe weather and mechanical breakdown to cargo damage and accidental marine pollution, the financial consequences of a maritime incident can be catastrophic.

To protect corporate balance sheets and maintain compliance with international shipping mandates, navigating the commercial risk market is a fundamental requirement. This guide breaks down the essential legal and financial frameworks governing marine insurance, evaluates localized coverage structures, and details how modern logistics operators secure their investments against maritime liabilities.

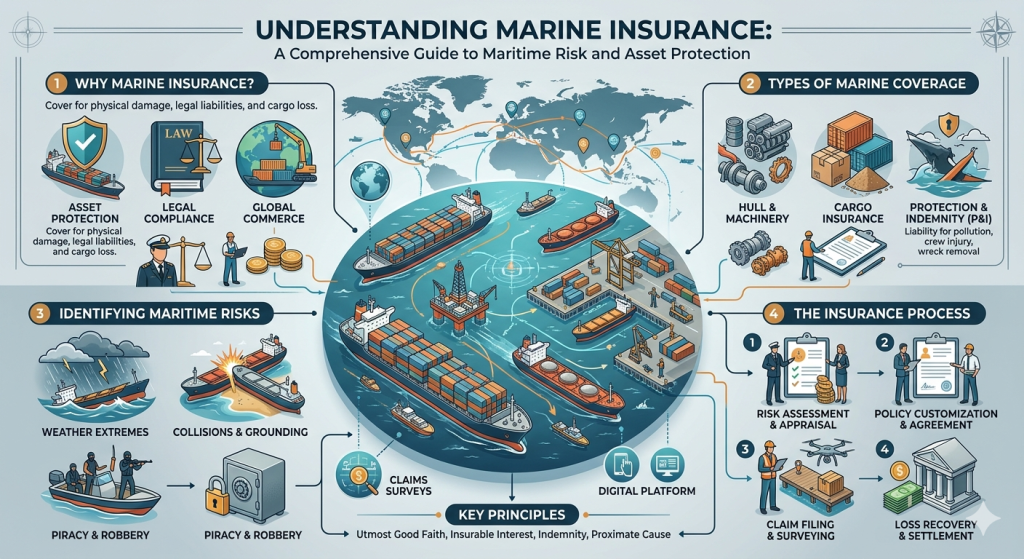

The Core Architecture of Marine Risk Mitigation

In the international shipping industry, risk management is split into distinct categories depending on whether the asset is a moving vessel, a floating cargo container, or terrestrial infrastructure. To properly structure a risk management portfolio, corporate procurement teams must understand the core insurance classes.

+——————————————————————-+

| PRIMARY MARITIME INSURANCE BLOCKS |

+———————————+———————————+

| HULL & MACHINERY (H&M) | PROTECTION & INDEMNITY (P&I) |

| • Insures physical ship asset | • Mutual third-party liability |

| • Covers collisions & grounding | • Covers oil spills & injuries |

+———————————+———————————+

|

v

+———————————+

| INLAND MARINE INSURANCE |

| • Covers cargo moving over land |

| • Bridges ports to inland hubs |

+———————————+

Hull & Machinery (H&M) Insurance

Hull and Machinery insurance serves as the baseline protection for the physical ship itself. This class of coverage indemnifies the shipowner or bareboat charterer against structural damage to the vessel’s hull, onboard propulsion systems, cranes, and specialized maritime machinery. H&M policies are critical for managing risks associated with heavy-weather transits, harbor collisions, and accidental groundings in shallow waterways.

Protection & Indemnity (P&I) Clubs

Unlike standard commercial insurance companies, marine insurance liabilities involving third-party risks are largely managed by specialized mutual associations known as Protection and Indemnity (P&I) Clubs. P&I coverage functions as an open-ended pool where ship operators mutually insure one another against high-impact risks, including:

- Accidental oil pollution and environmental remediation costs.

- Wreck removal obligations mandated by regional port authorities.

- Third-party property damage to docks, jetties, and loading arms.

- Crew injury, illness, or loss of life during offshore operations.

Decoupling Marine vs. Inland Marine Coverage

One of the most frequent points of confusion for logistics managers transitioning from land-based distribution to maritime shipping is separating ocean marine coverage from specialized inland marine insurance.

What is Inland Marine Insurance?

Despite its name containing the word “marine,” an inland marine insurance policy focuses heavily on land-based transportation networks. Originally developed to cover cargo once it was unloaded from a ship and moved inland via rivers or canals, modern inland marine coverage protects assets, equipment, and high-value commodities while they are in transit over land via trucks, trains, or specialized logistics vehicles.

Sourcing Inland Marine Insurance Coverage

Understanding the scope of inland marine insurance coverage is critical for companies managing intermodal supply chains. While an ocean marine policy protects cargo while it sits inside a vessel’s hold on open water, that coverage typically terminates once the container hits the terminal dock.

By working with certified inland marine insurance companies, exporters and importers can bridge this protection gap. This ensures their products remain fully covered against theft, accidental damage, or transit destruction while traveling from the coastal port to inland distribution centers, construction sites, or terrestrial warehouses.

Step-by-Step Risk Assessment for Maritime Charterers

Before signing a charterparty agreement or authorizing a high-value cargo loading sequence, corporate charterers should execute a structured risk verification protocol:

1.Execute a Complete Fleet Certificate Audit:Step 1.

Charterers must review the statutory documentation of the prospective vessel. This includes verifying that the shipowner maintains active, unrestricted coverage with a reputable P&I club and holds valid anti-pollution certificates. Operating with an under-insured or unvetted vessel leaves the charterer exposed to severe legal liabilities if an incident occurs.

2.Define Clear Cargo Liability Boundaries:Step 2.

Meticulously review the contract terms to establish exactly when cargo risk shifts from the seller to the buyer (utilizing standard Incoterms). Ensure a dedicated marine cargo policy is actively pinned to the transit window, explicitly detailing exclusions for specialized handling, temperature-controlled freight, or hazardous materials.

3.Verify Regulatory and Flag-State Compliance:Step 3.

Ensure the vessel and its crew comply directly with international safety frameworks like the ISM Code and local flag-state guardrails. In West African waters, this means confirming full compliance with regulatory bodies like NIMASA, ensuring all safety, security, and environmental protection certificates are up to date before mobilization.

Frequently Asked Questions (FAQ)

Q: What is inland marine insurance, and how does it differ from ocean marine insurance?

A: Ocean marine insurance is designed to protect physical vessels, hulls, and cargo while they are operating on open water, performing international transits, or sitting at maritime ports. In contrast, inland marine insurance protects high-value assets, equipment, and cargo while they are being transported over land via trucks or rail networks, or while they are temporarily stored at onshore logistics hubs.

Q: Why do maritime operators rely on P&I Clubs instead of traditional marine insurance companies?

A: Traditional commercial marine insurance companies operate for profit and typically cap their maximum liability limits, making them unsuitable for handling catastrophic third-party risks. P&I Clubs operate as non-profit mutual insurance cooperatives. By pooling resources globally, shipowners can secure the massive, flexible financial backing necessary to cover high-impact liabilities like major oil spills, wreck removals, and large-scale environmental damage.

Q: Does a standard marine cargo policy cover losses caused by shipping delays?

A: Most standard marine cargo insurance policies explicitly exclude financial losses resulting strictly from commercial or operational delays. Cargo policies are engineered to cover physical damage, theft, or total structural loss of the commodity caused by maritime perils (such as a vessel grounding or fire). If a charterer requires protection against market price fluctuations due to shipping delays, they must secure specialized, separate business interruption riders.

Q: What is a “General Average” clause in maritime transport risk?

A: General Average is a fundamental legal principle in maritime law. It dictates that if a captain intentionally sacrifices a portion of the cargo or incurs extraordinary expenses to save the vessel and the remaining cargo during an emergency (e.g., jettisoning containers to stabilize a grounding ship), all commercial parties involved in the voyage must proportionally share the financial loss. A robust marine cargo insurance policy will cover a charterer’s calculated General Average contribution.

Looking for Fully Vetted, Safe, and Compliant Vessel Chartering?

Oitha Marine provides reliable, operationally sound, and fully insured vessel chartering configurations across regional and international trading lanes. We prioritize strict compliance, ensuring every craft in our fleet maintains active P&I club coverage and adheres completely to NIMASA safety frameworks to protect your cargo and timeline from origin to destination. Contact our commercial logistics desk today at oithamarine.com to receive a prompt fleet overview or voyage estimate.

Recent Comments